The power of asset allocation might surprise you. Strategic asset allocation decisions alone explain over 75% of your portfolio’s return variability. Building wealth requires a solid understanding of investment distribution, especially if you’re over 40.

The classic “100 minus your age” rule guides many investors’ stock allocation decisions. This means putting 40% in stocks and 60% in bonds at age 60. But this simple formula represents just one strategy among many options. Research proves that your portfolio’s performance metrics improve by a lot when you add assets like real estate and commodities to your traditional mix. The right asset allocation strategy protects your wealth and enables growth during your prime earning and pre-retirement years.

Your financial experience after 40 demands a straightforward asset allocation model. Experts suggest that the six strategies we’ll explore help you build wealth more effectively than picking individual stocks or timing the market.

Strategic Asset Allocation

Image Source: Investopedia

Success in long-term investing depends on a well-laid-out approach to dividing your portfolio. Strategic asset allocation (SAA) ranks among the most powerful portfolio management methods accessible to investors over 40.

What strategic asset allocation is

Strategic asset allocation helps you think over a long-term approach to dividing investments across different asset classes based on your financial goals, risk tolerance, and time horizon. Unlike active approaches, SAA sets target percentages for various asset classes in your portfolio and maintains those allocations through periodic rebalancing.

This strategy is different from tactical approaches because it focuses on 5-to-10-year time horizons instead of short-term market movements. SAA requires you to determine your optimal mix of assets—typically stocks, bonds, real estate, and possibly alternative investments. You then systematically return to those target allocations when market movements cause them to drift.

Strategic asset allocation offers two main approaches:

- Fixed-target allocation (steady): Your portfolio maintains consistent proportions of global equities and bonds through regular rebalancing

- Time-varying allocation (dynamic): Your asset mix adjusts over time to optimize returns according to your portfolio’s objectives

Why strategic asset allocation works

Strategic asset allocation’s power comes from its comprehensive approach to diversification. Research shows 80–91% of a portfolio’s return variability stems from strategic asset allocation decisions alone. Your original allocation choices matter more than picking individual securities or timing the market.

Strategic asset allocation succeeds by using three critical elements:

- Each asset class’s unique risk-return profile

- Asset responses to economic factors like growth and inflation

- Correlation measurements between different asset classes to combine them efficiently

SAA prevents emotional decisions during market volatility. Clear allocation targets help you avoid making pricey mistakes like selling during downturns or chasing performance.

Strategic allocation spreads risk across assets with different characteristics. Equities and bonds typically have a negative correlation—one rises while the other falls—which creates a more stable overall portfolio.

How to implement strategic asset allocation

Your effective strategic asset allocation starts with answering key questions about your situation:

- What performance target do you want?

- How much loss can you handle?

- What liquidity needs do you have?

- Do you have specific timeframes (like retirement) or financial goals?

The next step determines your target allocations based on your risk profile and time horizon. To name just one example, see how an investor with higher risk tolerance might choose 80% equities and 20% bonds, while someone more conservative might prefer 40% equities and 60% bonds.

After setting your allocation, create a regular rebalancing schedule—typically annually. Market movements can cause allocations to drift substantially from targets. You’ll need to sell portions of overweight assets and buy underweight ones.

A 60-year-old investor with a conservative approach and five years until retirement might set up a 40/40/20 allocation (equities/fixed income/cash). With a €500,000 portfolio, they would start with €200,000 in equities, €200,000 in fixed income, and €100,000 in cash.

After one year, if equities grew 10%, fixed income returned 5%, and cash yielded 2%, the portfolio would drift to 41.3% equities, 39.5% fixed income, and 19.2% cash. Rebalancing would require selling about €6,870 of equities, buying €2,671 of fixed income, and adding €4,198 to cash.

Your strategic allocation should become more conservative as you age, especially after 40. Many financial advisors recommend the Rule of 110—subtract your age from 110 to find your approximate equity percentage.

Constant-Weighting Asset Allocation

Image Source: Investopedia

Market changes can throw your carefully planned asset mix off balance. The quickest way to handle this is through constant-weighting allocation. Many investors over 40 find this approach valuable. The challenge is simple – market movements will naturally change your planned asset proportions if you don’t take action.

What constant-weighting asset allocation is

Constant-weighting asset allocation (also called “constant mix” or “constant ratio plan”) keeps fixed proportions of aggressive and conservative assets in your portfolio through systematic rebalancing. This approach differs from strategic allocation’s buy-and-hold method. You need to adjust your portfolio continuously when market movements push your asset proportions away from their original targets.

This strategy works by setting target weights for each asset class in specific tolerance ranges, or “corridors”. To name just one example, you might aim for 30% in emerging market equities, 30% in domestic blue chips, and 40% in government bonds. Each asset class could fluctuate by ±5%. The portfolio needs rebalancing back to its original allocation when any asset class moves beyond its predetermined band.

The approach works through these steps:

- Setting fixed target percentages for different asset classes

- Creating tolerance ranges for acceptable drift

- Starting rebalancing when allocations go beyond these ranges

- Keeping consistent risk exposure whatever your wealth level

Why constant-weighting asset allocation works

This strategy works best in volatile markets that show mean-reverting patterns. You can take advantage of natural market cycles by selling assets that perform well and buying underperforming ones. This approach puts the “buy low, sell high” principle into action.

On top of that, this strategy brings several key benefits:

- Automatic rebalancing provides protection against slow responses to market trends. The portfolio adjusts quickly to changing market conditions through automatic rebalancing

- Emotional discipline: You remove emotional decision-making during market volatility with preset rebalancing rules

- Profit-locking: You secure gains by selling portions of assets that reach target levels

- Counter-cyclical adjustments: Your investment returns can smooth out over longer periods by moving against market momentum

Notwithstanding that, constant weighting isn’t always better than other strategies. Research indicates that some investors—especially those who need a minimal subsistence level—might do better with buy-and-hold approaches in certain situations. I love that as your investment horizon increases, more investors may prefer buy-and-hold strategies over constant allocation.

How to implement constant-weighting asset allocation

You’ll need clear parameters and a disciplined rebalancing process to implement this strategy:

- Choose your target allocation mix based on your risk tolerance, time horizon, and financial goals

- Set tolerance bands for each asset class (usually ±5% from original targets)

- Keep an eye on your portfolio to spot when assets drift beyond tolerance bands

- Complete rebalancing trades as needed by selling overweight assets and buying underweight ones

Your tolerance bands’ optimal width depends on three factors: transaction costs, price volatility, and correlation with other holdings. Assets with higher transaction costs need wider bands to reduce trading expenses. However, highly volatile securities should have narrower bands to stay properly represented in your portfolio.

You can choose between calendar-based intervals or corridor-based triggers for rebalancing. Many investors rebalance when any asset class moves more than 5% from its target. Some mutual funds now offer automatic rebalancing features that handle these adjustments for you.

Constant weighting gives investors over 40 a disciplined way to maintain their desired risk level as retirement approaches. This helps protect your wealth while still allowing room for growth.

Tactical Asset Allocation

Image Source: Finance Strategists

Smart investors look beyond fixed models to get better returns through dynamic approaches. Tactical asset allocation (TAA) shows this move in thinking—you adjust your portfolio temporarily to take advantage of short-term market chances or guard against potential losses.

What tactical asset allocation is

Tactical asset allocation actively manages portfolio strategy by temporarily moving asset percentages in different categories to profit from market pricing anomalies or strong market sectors. Unlike strategic or constant-weighting approaches, tactical allocation works in shorter investment windows—usually 3 to 12 months.

You’ll get extra returns through asset allocation adjustments rather than picking individual securities. TAA lets you keep your long-term strategic allocation as a base while making calculated short-term changes based on current market conditions.

You can use two distinct methods for tactical allocation:

- Discretionary TAA: You adjust asset allocation based on market valuations and expected changes

- Systematic TAA: Quantitative investment models help find temporary imbalances between different asset classes

These tactical moves don’t last forever—you go back to your original strategic allocation once the short-term chance disappears or you hit your target.

Why tactical asset allocation works

Markets aren’t always perfectly efficient, which makes tactical asset allocation effective. Research shows it can beat market returns by using several market features:

- Market segments and structural roadblocks

- How information flows and behavioral differences

- Investors with non-profit motives

- Gaps between markets and asset classes

TAA offers practical benefits for investors over 40. You get flexibility to respond to market changes instead of following a fixed plan. Your tactical decisions can work alongside long-term strategic choices.

Risk management becomes easier with tactical allocation. You can pull back from risky assets during tough times to protect your portfolio. This approach matters more as your wealth grows in your 40s and 50s, when protecting your money becomes crucial.

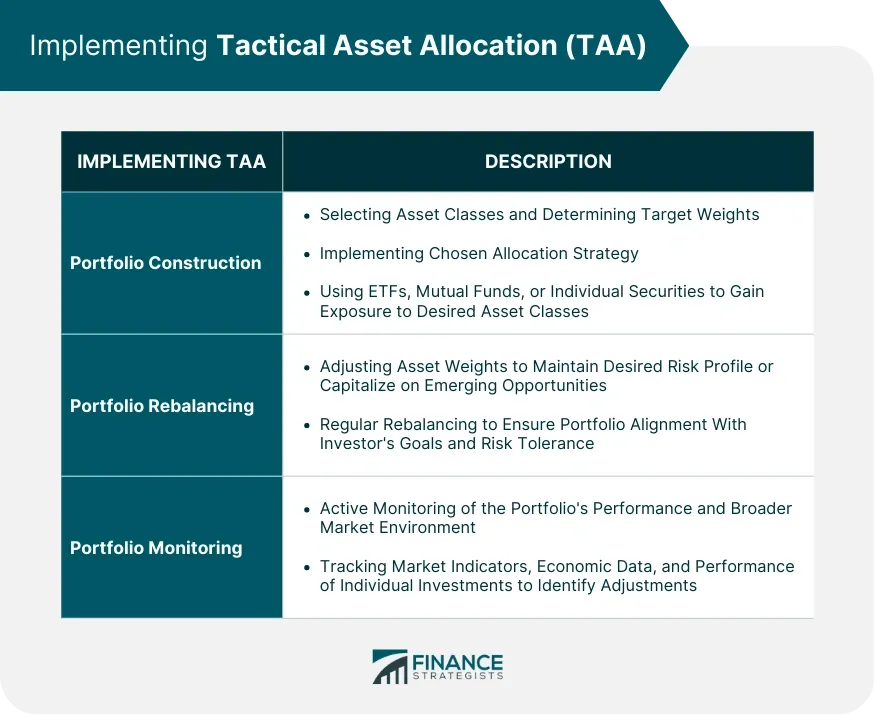

How to implement tactical asset allocation

A successful tactical allocation strategy needs both discipline and method:

- Build a strong strategic allocation as your foundation

- Watch market conditions and economic signs to spot potential chances

- Find specific tactical opportunities where short-term changes might help

- Make small tactical moves—usually 5% to 10% of your total allocation

- Know when to exit and return to your strategic allocation

Look for big economic shifts, value differences between markets, or technical signs showing momentum changes. Strong growth in one sector might lead you to increase your money there temporarily.

Here’s a real example: Your strategic plan might have 50% stocks, 30% bonds, and 20% cash. You see tech stocks looking strong. You could move to 60% stocks (with more technology), 20% bonds, and 20% cash for 3–6 months before returning to your original mix.

Note that tactical asset allocation doesn’t mean big changes or constant trading. Even top institutional managers keep tactical moves between 5–10% of their total allocation. Too much trading cuts back on returns through costs and taxes.

For investors over 40, tactical allocation strikes a balance between strict long-term planning and reactive market timing. This approach helps build wealth while keeping risks in check.

Dynamic Asset Allocation

The value of managing your portfolio responsively grows as markets swing and economic conditions shift. Dynamic asset allocation gives investors over 40 a framework that adapts their investments to market realities.

What dynamic asset allocation is

Dynamic asset allocation lets portfolio managers adjust their mix of asset classes based on changing market conditions. This approach stands apart from strategic or constant-weighting methods. Portfolio managers don’t stick to specific target mixes, which allows them more room to make investment decisions.

The strategy works by cutting back on poorly performing assets while putting more money into stronger ones. Dynamic allocation creates a framework for ongoing portfolio changes based on economic and financial market trends, unlike tactical allocation, which chases short-term gains.

The mix of stocks and bonds in your portfolio may change based on the following factors:

- Overall economic health

- Specific sector performance

- Bear or bull market conditions

This strategy responds to market risks and downturns. It also spots emerging trends that could beat standard return targets.

Why dynamic asset allocation works

Your portfolio adapts to market changes instead of staying fixed with dynamic asset allocation. This flexibility brings several benefits:

- Better returns potential: Quick adjustments to your asset mix could lead to higher returns. You can dodge unexpected market drops while riding the wave of rising sectors.

- Risk management: Your portfolio loses less during downturns because you reduce exposure to weak assets.

- Diversification benefits: Strong sectors can balance out weaker ones when you spread investments across multiple asset classes.

- Market responsiveness: Your portfolio can quickly adapt to new market conditions and risks, unlike static allocations.

Without doubt, putting more money in top-performing asset classes keeps your portfolio’s momentum high. This could mean extra returns if positive trends continue. You also cut potential losses during market corrections by reducing holdings in declining assets.

How to implement dynamic asset allocation

You need a systematic approach and constant market reviews to make dynamic asset allocation work:

- Review current conditions: Look at how each asset class performs, including equity values and interest rate trends.

- Adjust weightings: Put more money into strong performers and less into weak ones based on your review.

- Monitor key metrics: Monitor interest rate cycles, equity values, and the longer-term asset class outlook.

- Set parameters for changes: Please establish clear guidelines regarding the timing and extent of adjustments to your allocations.

Let’s take a real example: Global equities enter a six-month bear market. You might shift money from stocks to bonds to protect against risk. A stock-heavy portfolio could sell some equities to buy more bonds. Later, improving economic conditions might signal the time to increase stock holdings again.

Dynamic asset allocation comes with its challenges. You’ll pay more in transaction costs from frequent trading, which could eat into returns. The strategy also needs time, resources, and market knowledge to work.

Investors over 40 who build retirement wealth will find dynamic asset allocation hits the sweet spot. It offers more flexibility than rigid approaches but more structure than day trading.

Insured Asset Allocation

Many risk-conscious investors nearing retirement want to protect their wealth rather than chase aggressive growth. Insured asset allocation emerges as a safety-focused strategy that sets clear boundaries around potential losses while letting you manage your portfolio actively.

What insured asset allocation is

Your investments need a safety net. Insured asset allocation creates this by setting a base portfolio value that becomes your protective floor. This strategy lets you grow your wealth when markets are strong. The approach combines active management with risk control to protect what you’ve built.

The basic principle makes sense. You pick a minimum value for your portfolio and take action whenever your investments get close to this boundary. This method appeals to investors who want to preserve their capital but still want to manage their portfolio actively.

Insured asset allocation works differently from other strategies with two main modes:

- Above the floor: Your portfolio value exceeds the base, so you participate in active management to maximize returns

- At the floor: Your portfolio approaches the minimum threshold, so you move to capital preservation through risk-free assets

Why insured asset allocation works

The strategy succeeds because it gives investors peace of mind through guaranteed minimums. Risk-averse investors over 40 find this approach helpful to protect their wealth as they get closer to retirement. Yes, it is a way to maintain your lifestyle during retirement by keeping your portfolio above a set value.

The strategy’s strength comes from its dual nature. Strong markets let you benefit from active management and growth. Market downturns trigger protective measures before losses become severe. This safety net stops major market crashes from destroying your retirement plans.

Clear decision-making rules are the foundation of this strategy. Market volatility won’t force emotional reactions because you follow set rules about moving toward safer investments. This method has behavioural biases, which often result in poor investment timing.

How to implement insured asset allocation

You need these key steps to create an effective insured asset allocation strategy:

- Determine your base portfolio value – Pick the lowest acceptable value for your investments based on your retirement needs

- Establish your active management approach – Plan how you’ll handle investments above the floor value using research, forecasts, and experience

- Identify your risk-free assets – Choose safe investments like Treasury bills to use when your portfolio nears the floor value

- Create clear trigger points – Set exact levels that signal when to move from active management to preservation

- Develop a consultation plan – Get professional help to move assets if your portfolio hits the floor value

Here’s a real example: A $1 million portfolio with an $800,000 base value lets you manage investments actively while staying above this threshold. If market drops push your portfolio toward $800,000, you move assets into Treasury bills and other safe investments to stop further losses.

Building wealth after 40 becomes easier with insured asset allocation. The strategy balances peace of mind with growth potential – perfect for people close to retirement who can’t risk big losses but still need their money to grow.

Integrated Asset Allocation

A complete framework emerges when you blend multiple asset allocation methods together. This approach goes far beyond basic strategies. Investors over 40 who want both structure and flexibility in their wealth-building experience will find integrated asset allocation represents the next step in portfolio management.

What integrated asset allocation is

Integrated asset allocation merges strategic and tactical methods while taking into account your risk comfort level, market conditions, and other vital factors. This mixed strategy doesn’t just look at long-term goals or quick opportunities separately. It creates stability through long-term planning and stays flexible with short-term tactics.

This method is unique in that it considers both your economic expectations and your risk tolerance when choosing assets. The approach gives you a clear way to see all the key parts of your asset allocation decisions by bringing together different strategies.

The main focus stays on growing your total worth instead of managing separate investment accounts. This bigger picture looks at everything you own minus what you owe, plus how much these numbers might change over time.

Why integrated asset allocation works

The success of integrated asset allocation comes from its ability to connect investment returns with ground impact. You can measure and control both risk and performance across your whole investment portfolio with this complete approach.

This method proves its worth through a balanced viewpoint. It stays true to long-term goals while making smart changes to boost returns. The strategy helps you direct your way through market ups and downs without losing sight of your basic money goals.

Most allocation strategies look at future market returns, but not all think about how much risk investors can handle. This two-sided approach makes integrated allocation perfect for building wealth after 40, when protecting what you have becomes just as important as growing it.

How to implement integrated asset allocation

You can implement integrated asset allocation by following these steps:

- Turn your current net worth into risk tolerance using a special calculation

- Look at current market conditions including prices, earnings, and dividends, to figure out expected returns and risks for different types of investments

- Pick the right mix of assets using tools that look at both your risk comfort and market forecasts

- Check and change things as your returns affect your worth and markets shift

To name just one example, you might start with a long-term plan but adjust it based on your changing money goals, economic conditions, and market trends. This flexibility lets you stay stable while taking advantage of new opportunities.

Integrated asset allocation gives investors over 40 a powerful tool that balances structure with adaptability. It combines long-term planning with quick responses to help build wealth most effectively.

Age-Based Asset Allocation Strategy

Image Source: Financial Edge Training

Your age means more than just a number—it’s a beneficial way to structure your investment portfolio. Age-based asset allocation gives you a simple yet effective way to manage investments. We focused on matching your portfolio risk with your life stage.

What age-based asset allocation is

Age-based asset allocation follows a basic principle: your investment risk should decrease with age. The strategy uses a simple formula to find your ideal stock allocation—subtract your age from 100, 110, or even 120 to calculate your equity percentage. For example, if you are 45 years old and apply the rule of 110, you would allocate approximately 65% of your investments to stocks and the remaining 35% to bonds and cash.

This strategy is different from others because it uses your age as the main factor for risk exposure rather than market conditions or tactical opportunities. Your investments naturally move from growth-focused options toward more conservative ones as time goes by.

Why age-based asset allocation works after 40

Your peak earning years usually start after 40, and you might have more financial freedom as your family’s needs decrease. T. Rowe Price’s largest longitudinal study shows that by 45, you should have saved three times your current income for retirement. This amount should increase to five times your current income by age 50 and seven times by age 55.

Retirement could last three decades or more, so your portfolio needs room for growth. However, your risk tolerance naturally drops as retirement gets closer—you have less time to bounce back from major market downturns.

How to implement age-based asset allocation

Here’s how to implement age-based allocation properly:

- Maximize retirement contributions — Make use of catch-up contributions when you turn 50

- Gradually shift toward conservatism — Keep enough stocks for growth while adding more bonds and cash positions

- Rebalance regularly — Think over starting systematic transfer plans (STPs) to smoothly move investments from equity to debt funds

The most important step is keeping an emergency fund that covers 3-6 months of expenses. This helps keep your financial goals on track. Age-based allocation gives you a straightforward yet effective strategy to build wealth beyond 40 when you balance current needs with future goals.

Comparison Table

| Strategy | Main Goal | Time Horizon | Key Characteristics | Main Advantages | Implementation Approach |

| Strategic Asset Allocation | Long-term structured approach based on financial goals | 5-10 years | Target percentages stay steady through regular rebalancing | This strategy explains 80-91% of portfolio return changes | Set target allocations based on risk profile and rebalance yearly |

| Constant-Weighting Asset Allocation | You retain control of fixed proportions through systematic rebalancing | Ongoing | Uses range limits for each asset class | Works well in volatile markets with mean-reverting patterns | Set fixed targets with ±5% tolerance bands and rebalance when exceeded |

| Tactical Asset Allocation | Short-term market opportunities | 3-12 months | Temporary changes in asset percentages | Lets you respond quickly to market changes | Make small tactical moves (5-10%) based on market conditions |

| Dynamic Asset Allocation | Portfolio adjustments follow market conditions | Variable | Regular adjustments without specific target mix | Better returns potential and risk control | Cut down positions in weaker assets while increasing stronger ones |

| Insured Asset Allocation | Protection of base portfolio value | Long-term | Sets minimum threshold value | Stops big losses while allowing growth potential | Set a base value and move to risk-free assets when approaching the floor. |

| Integrated Asset Allocation | Complete wealth management | Both short- and long-term | Combines strategic and tactical approaches | Looks at both risk tolerance and market conditions | Change net worth into risk tolerance and optimize asset mix |

| Age-Based Asset Allocation | Risk reduction with age | Lifelong | Uses age-based formulas (e.g., 110-age) | Easy to understand and use | Move from growth to conservative investments as age increases |

Conclusion

Asset allocation is the lifeblood of successful investing after 40. Expat Wealth At Work explores six distinct strategies that balance growth potential with risk management. These strategies go beyond theory and provide practical frameworks you can use.

Your investment experience after 40 is different from your earlier years. You now have substantial accumulated assets and time to grow your wealth further. The right allocation strategy becomes significant to protect your assets while continuing to build wealth.

Strategic and constant-weighting allocations give disciplined approaches that long-term investors need for stability. Tactical and dynamic strategies let you adapt to changing market conditions. On top of that, insured allocation creates safety nets when capital preservation matters most. Integrated approaches merge multiple methods for complete wealth management.

Age-based allocation is the most straightforward option, maybe even the simplest. It automatically adjusts your risk exposure as retirement approaches. This simplicity makes it a popular choice among investors who want uncomplicated solutions.

Note that no single strategy works for everyone perfectly. Your personal risk tolerance, time horizon, and financial goals will determine the best approach for you. Many successful investors blend elements from multiple strategies to create their own frameworks.

The comparison table we shared earlier helps evaluate which strategy matches your situation. Whatever path you choose, applying a well-laid-out asset allocation strategy is nowhere near as risky as picking individual winners or timing market movements.

Building wealth after 40 requires both protection and growth. These six allocation strategies are proven frameworks to achieve both goals at once. A clear allocation strategy that fits your financial situation makes your investment experience substantially easier to manage.