The question intrigued us for years – why invest when you could keep your money secure in a bank account? We watched our savings grow painfully slowly at less than 1% per year. Meanwhile, inflation continued to erode the value of our savings. Keeping all your money in savings makes you poorer as time passes.

“Why Invest?” is more than just a question; it unlocks the path to financial independence. The data presents a compelling narrative. Savings accounts have averaged tiny returns of 0.06%, while the S&P 500 has given annual returns of about 10% in the last century. Many people still feel nervous about starting to invest, despite this huge difference.

Expat Wealth At Work explains the basic reasons to invest, investment options you can choose in 2026, and how compound interest can turn small regular deposits into wealth. You’ll learn why common investment myths hold no truth and get practical ways to start investing, even with a small amount of money.

Investing isn’t about quick profits or chasing market trends. It helps build wealth through smart choices and patience. You can start this trip from any point.

Why Invest? Understanding the Real Reason Behind It

People often misunderstand the true reason behind investing. Many start their investment journey after hearing tales of overnight millionaires or worry they might miss the next big chance. However, the primary motivation for investing is not to become wealthy quickly.

Fear of missing out vs. long-term planning

FOMO (fear of missing out) guides investors toward poor choices. Our friends have rushed into “hot stocks” or cryptocurrencies when prices peaked, then sold everything in panic as values dropped. This emotional approach yields results nowhere near market performance.

A focus on long-term planning builds wealth gradually through steady contributions and compound growth. Smart investors create diversified portfolios that line up with their financial goals and time horizons instead of chasing trends.

How inflation erodes savings

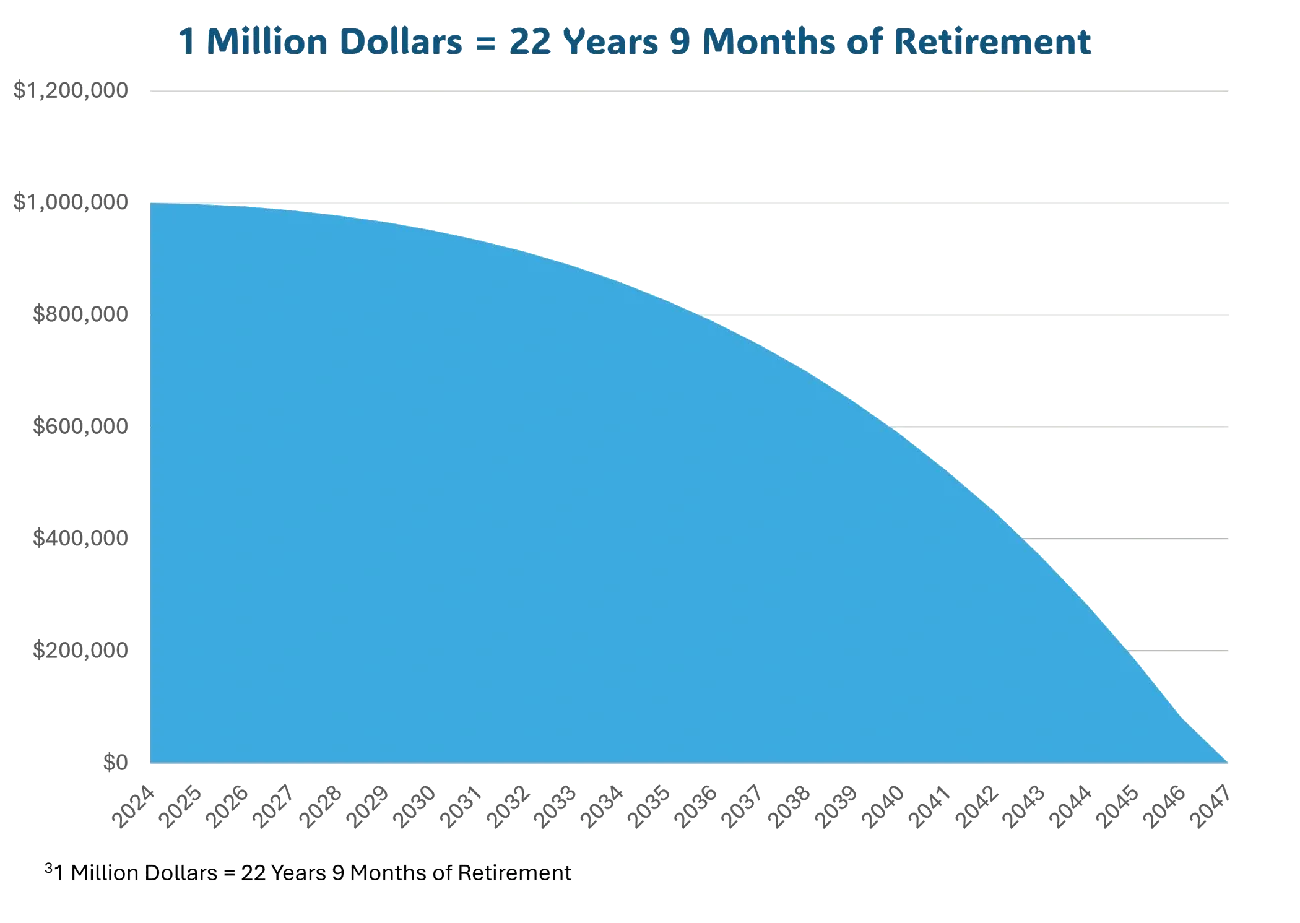

Your money’s value silently drops year after year due to inflation. The math tells a clear story: $100,000 today shrinks to just $55,368 in 20 years with 3% inflation. That $5 morning coffee could cost $9 two decades from now.

Money in traditional savings accounts earning tiny interest (0.01% to 0.5%) loses value steadily. The historical average inflation rate of 3% grows faster than most savings account returns, which makes saving alone inadequate to preserve wealth.

The mindset shift from saving to investing

The change from saving to investing needs a fundamental mental adjustment. Savers place capital preservation above everything else and avoid risks that could fuel growth. Investors know calculated risks bring meaningful returns.

This change happens only when we are willing to see how “safety” brings its own risk—falling behind. When we realised that our “safe” savings accounts guaranteed less purchasing power each year, the truth became clear.

Investing serves a deeper purpose than getting rich—it prevents poverty over time. It protects and grows your purchasing power against inflation while building wealth that supports your long-term financial goals.

Types of Investments You Should Know in 2026

The financial world of 2025 rewards smart money decisions that can make the difference between thriving and just getting by. Let’s look at the best ways to invest your money right now.

Stocks and ETFs

Individual stocks provide you with ownership in specific companies and can yield significant returns, but you must conduct thorough research. Exchange-Traded Funds (ETFs) give you a simpler choice—they work like baskets of securities that track indexes, sectors, or themes. To name just one example, an S&P 500 ETF spreads your investment across America’s 500 largest companies automatically. ETFs cost less than mutual funds, which makes them perfect for newcomers who want broad market exposure.

Real estate and REITs

Physical property remains a fantastic way to build wealth, but you’ll need deep pockets and management skills. Real Estate Investment Trusts (REITs) let you invest in real estate without buying actual property. These companies own or finance income-producing real estate in a variety of sectors—from residential buildings to data centres. REITs must give shareholders 90% of their taxable income as dividends, which often leads to better yields than most stocks.

Cryptocurrencies and digital assets

The digital asset world now goes beyond Bitcoin and Ethereum to include stablecoins, NFTs (non-fungible tokens), and DeFi (decentralised finance) platforms. These assets offer state-of-the-art potential for growth but come with higher risks. Our advice? Keep only 5-10% of your portfolio here and stick to well-established cryptocurrencies instead of risky alternatives.

Bonds and fixed income

Bonds are basically loans to governments or corporations that pay you regular interest. Treasury bonds, municipal bonds, and corporate bonds each come with their own risk and return profiles. Interest rates have stabilised in 2025, and bonds are back to their old job of steadying portfolios while providing reliable income.

Alternative investments (art, collectibles)

Physical assets like fine art, rare coins, vintage cars, and luxury watches can help you vary beyond regular markets. New platforms let you own small pieces of these once-exclusive assets. Notwithstanding that, these investments need special knowledge and longer holding times. Think of them as passion projects that might grow in value rather than core investments.

The Truth About Building Wealth Through Investing

Building lasting wealth through investing isn’t about picking hot stocks or timing the market. It’s about understanding a few basic principles that wealthy people have used to grow their money for generations.

Why time in the market beats timing the market

Smart investors know that being consistent works better than trying to time things perfectly. Research shows that if you miss just the 10 best trading days over 20 years, your returns could drop by half. In fact, investors who stayed put during market downturns did better than those who jumped in and out. This is why Warren Buffett famously said his favourite holding period is “forever”.”

The power of compound interest

Albert Einstein called compound interest the eighth wonder of the world—and with good reason too. The growth looks small at first but becomes amazing over time. A $10,000 investment with 10% annual returns grows to $25,937 after 10 years and reaches $67,275 after 20 years. Most of this growth happens in later years, which makes starting early so significant.

How diversification reduces risk

Diversifying your investments across various asset classes serves as a strategy to mitigate risk. When stocks aren’t doing well, bonds or real estate might be performing better. Your properly diversified portfolios have historically earned 70–80% of the market returns with substantially less volatility.

Common myths that hold people back

Many think they need a lot of money to start investing, but many platforms let you begin with just $5. Some people wait for the “perfect time” to invest. They don’t realise that spending time on the market matters more than perfect timing. It also helps to know that disciplined, research-based investing is different from gambling.

These basic truths about investing are the foundations for building substantial wealth, whatever your starting point may be.

How to Start Investing (Even with Little Money)

You don’t need a fortune to start investing. The barriers to entry have fallen dramatically, and investing is more available than ever.

Choosing the right investment platform

Beginner-friendly apps let you trade with zero commission and minimal starting requirements. Robo-advisors will automatically build diversified portfolios based on your risk tolerance. Expat Wealth At Work gives you both automated investing and customised options to help you learn and maintain control.

Setting financial goals

Your first step before investing should be to determine your purpose. Short-term goals (1–3 years) need different strategies than long-term objectives (10+ years). Ambitious targets can motivate you to act, but SMART goals (specific, measurable, achievable, relevant, and time-bound) give you clarity and help track your progress.

Automating your investments

After picking a platform and setting your goals, you should set up recurring transfers from your checking account. This “pay yourself first” approach keeps your investments consistent whatever the market conditions. Dollar-cost averaging through automatic contributions helps smooth out market volatility over time.

Avoiding high fees and hidden costs

Expense ratios, management fees, and trading commissions can quietly eat away at your returns. Low-cost index funds with expense ratios under 0.2% should be your priority. On top of that, watch for account maintenance fees, inactivity charges, and transfer costs that can affect long-term performance, especially with smaller investment amounts.

Final Thoughts

Making investment decisions is vital for anyone who wants to maintain their purchasing power and build long-term wealth. This article shows how inflation quietly erodes savings while proper investments provide the growth you need to stay ahead. The trip from saver to investor involves calculated risks, but these risks become manageable by a lot through diversification and patience.

Time works better than timing for investment success. Compound interest’s mathematics works like magic but only shows its exponential potential after many years. Waiting for the “perfect moment” to invest guides you to missed opportunities and lower returns.

The financial landscape in 2026 offers more available entry points than ever. You can build a portfolio that matches your specific goals and risk tolerance with minimal capital requirements and user-friendly platforms. It also helps that automated investing tools remove emotional decision-making and create a disciplined approach even for beginners.

Fear stops many potential investors, but investing is different from speculation – the distinction brings clarity. Building sustainable wealth needs consistent contributions, diversification, and patience to ride out market changes instead of reacting to short-term swings.

Before you start your investment journey, discover what Expat Wealth At Work can offer you; our tailored approach may be just what you need to align your financial strategies with your life goals.

Financial freedom starts with a single step – your first investment. Market movements will happen without doubt, but properly diversified portfolios have historically moved upward. Consistent, informed investing remains the quickest way to create lasting wealth. Your future self will thank you for starting today.