Your retirement planning mistakes might rob you of decades of financial security. Most retirees wish they had planned their retirement differently.

The consequences of inadequate planning can be severe. All but one of the retirees had to quit working earlier than planned because their health failed or their company downsized. The numbers look even worse when you learn that only 25% have saved up one year’s worth of income to retire.

Retirement could stretch across 20 to 30 years – that’s a third of your life without steady paycheques coming in. Young professionals in their 20s and 30s often put off saving money. They miss out on compound interest’s amazing growth potential.

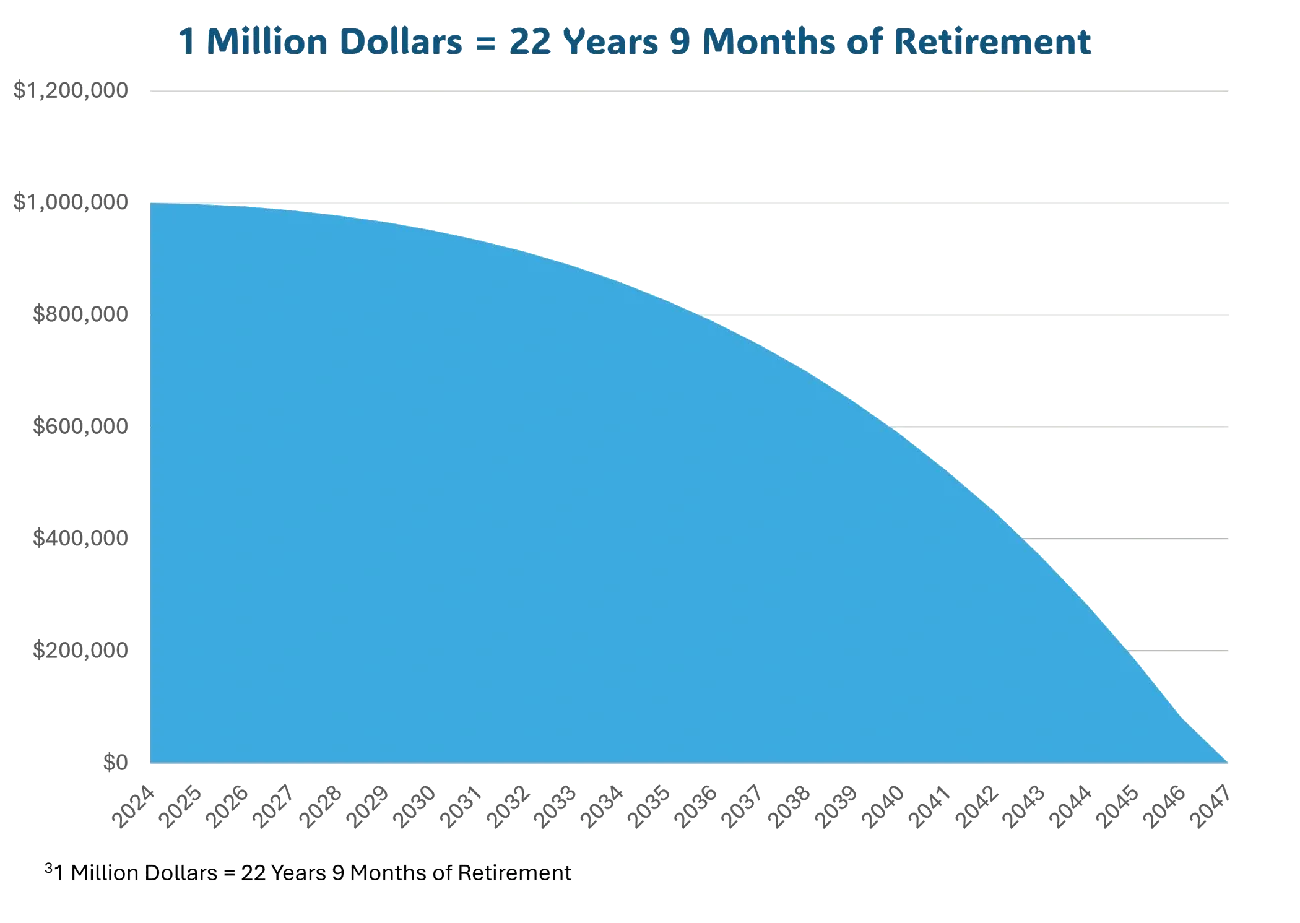

Expat Wealth At Work will help you dodge the retirement planning traps that could wreck your golden years. Long-term care costs run about €2,495 monthly. Social Security pays just €1,783 per month on average. These numbers show why you need a solid plan.

Not Saving Early Enough

People often underestimate what starting early retirement savings can do for them. Many hit their 40s or 50s and realise they’ve made one of the biggest retirement planning mistakes—putting off their savings. Approximately 1 in 5 individuals over 50 have not made any retirement savings, and over half express concern about their insufficient savings.

Not Saving Early Enough Explained

Not saving early enough means delaying retirement contributions during your 20s and 30s, when long-term investing is at its most effective. Several factors lead to this common mistake:

- Retirement seems too far away to act now

- Today’s expenses take priority over future needs

- Not realizing how much retirement will cost

- Missing out on how compound interest works

If you have people under 25, their average retirement savings are just €7,014.40, with a median of €2,687.06. These low numbers reflect both smaller paycheques and the tendency to put off saving. This delay comes with a hefty price tag.

Why Not Saving Early Enough Is a Mistake

Delaying retirement savings has significant financial consequences. Starting late means giving up your strongest wealth-building tool: compound interest.

Let’s look at this eye-opening comparison: Start investing €95.42 monthly at a 12% annual return compounded monthly for 40 years, and you’ll build up over €1.12 million. However, if you wait 30 years and then invest €954.21 monthly (ten times as much) for 10 years at the same rate, you will accumulate approximately €219,468.33.

This giant gap exists because compound interest grows exponentially—your interest makes more interest. This process creates a snowball effect that builds your retirement fund faster over time.

On top of that, starting late means:

- You’ll have to put in much more to hit the same targets

- You’ll lose years of employer matching contributions

- You won’t have enough time to bounce back from market drops

- You’ll miss out on tax benefits that add up over decades

The financial implications are significant. Someone who puts away €5,725.26 yearly starting at 20 could have almost €1.62 million by 60 (with an 8% return). Start at 40, and you’d only have about €282,446.19—that’s €1.34 million less.

How to Avoid Not Saving Early Enough

Young people have a simple solution: start now. Even small amounts can grow into something big over time. If you’ve waited, don’t worry—you’ll just need to be more aggressive:

Start with your employer’s retirement plan: Your employer’s match is free money—grab it.

Automate your savings: Most employers now put new employees into retirement plans automatically. About two-thirds of big employers do this. If your employer does not offer this, you may wish to consider setting up automatic transfers on your own.

Increase contributions gradually: Bump up your contribution by 1% each year, especially after raises. That’s just €47.71 more monthly for someone making €57,252.61 a year.

Tax advantages are your friend: Put money in tax-advantaged accounts. This arrangement cuts your taxable income and lets investments grow tax-free.

Consider the option of working longer if you are behind on your savings. Working until 70 instead of 62 could add more than €255,728.31 to your nest egg.

Late starters should aim to save 15-20% of their income for retirement. Financial experts say you’ll need at least €0.95 million in savings for a comfortable 30-year retirement.

Waiting just five years to start means paying €48,103.64 more for the same retirement outcome. A 25-year-old saving €100 monthly until 65 would pile up €175,500 (after putting in €51,600). Start at 40 with €200 monthly and you’d end up with €117,000 (after investing €60,000).

Early saving brings more than money—it gives peace of mind. Early savers feel less financial stress later and have more choices about when and how to retire. They also build money habits that help their overall financial health.

Note that the best time to start saving was yesterday. The next best time is today.

Not Having a Retirement Spending Plan

Retirees often spend decades saving money for retirement. Yet many reach their golden years without a clear strategy to turn savings into steady income. Recent data shows that 49% of retirees spend more than they planned, up from 36% in 2024. This financial gap exists because people fail to create a detailed retirement spending plan.

Not Having a Retirement Spending Plan Explained

A retirement spending plan serves as a roadmap to convert your saved assets into regular retirement income. The key parts of this plan include:

- Essential versus optional expenses

- Setting up safe withdrawal rates from retirement accounts

- Building a “retirement pay cheque” from different income sources

- Ways to handle market ups and downs and inflation

- Adjusting expenses through retirement stages

Retirees who put together a formal spending plan feel more confident about their retirement. Yet most people save for years without understanding how to use their savings effectively when the time comes.

This phenomenon happens because switching from saving to spending means changing habits built over a lifetime. As a result, retirees either spend too little and miss out on life’s pleasures or spend too much and risk running out of money.

Why Not Having a Retirement Spending Plan Is a Mistake

Life without a clear spending strategy brings several risks:

Your savings might run dry too soon. Running out of money ranks among retirees’ biggest fears. Taking out too much money too early can leave you short when you need it most—especially later in retirement when healthcare costs rise.

You might spend too little. Many successful retired investors barely touch their savings because they’re unsure about safe spending amounts. About 25% of retirees cut their spending during retirement. Such behaviour means missing out on retirement dreams and leaving wishes unfulfilled.

Changes become harder to handle without a plan. The first year brings the biggest money shifts as regular paycheques stop. Expenses also change throughout retirement—usually higher in early years (more activities) and later years (more healthcare).

Money decisions become emotional rather than logical. Financial advisors point out that overspending often comes from “emotional spending, lifestyle creep, or having no plan.”

How to Avoid Not Having a Retirement Spending Plan

A solid retirement spending plan needs these key steps:

- Break down your budget: Split expenses between “must-haves” (housing, food, healthcare, utilities) and “nice-to-haves” (travel, hobbies, dining out). This difference helps match basic needs with guaranteed income like Social Security and pensions.

- Set withdrawal rules: The classic 4% rule suggests taking 4% of retirement savings in year one, then adjusting for inflation. We recommend keeping initial withdrawals at 4%–5%. Think about whether this works for you or try other approaches, like:

- Fixed-euro withdrawals

- Percentage-based withdrawals

- Income-only withdrawals

- “Bucket” strategy (dividing money for short-, medium-, and long-term needs)

- Stay flexible: Your retirement budget will change over time. Financial experts assert that individuals’ spending patterns are not linear. Rather than strict rules, use spending ranges that let you adjust month to month.

- Map out retirement phases: We suggest breaking retirement into distinct stages with different spending patterns. Regular budget reviews help make savings last and bring peace of mind.

- Check quarterly: Track spending by category and watch for changes in patterns. This feature helps you spot needed adjustments to keep your plan working.

The goal isn’t perfect prediction. You need a framework that lets you enjoy retirement while keeping your money safe throughout your non-working years.

Ignoring Inflation in Retirement Planning

Image Source: STRATA Trust Company | SDIRA Services | Alternative IRA Custodian

Inflation acts as a hidden threat that slowly eats away at your retirement savings. 92% of retirees worry about inflation reducing their assets’ value. Many retirement plans don’t properly address this economic reality.

Ignoring Inflation in Retirement Planning Explained

Not factoring inflation into retirement planning means you overlook how rising prices will cut into your purchasing power during retirement. Inflation shows how much more you’ll pay for goods and services each year. Global governments aim to maintain inflation at 2%, but it can fluctuate significantly, as demonstrated by the 9.06% increase in June 2022.

Your money buys less over time, even with modest inflation rates. To name just one example, see how 2% inflation cuts your money’s value in half after 35 years. This decline in buying power hits retirees hard because they:

- Mostly live on fixed incomes

- Can’t easily earn more money

- Pay healthcare costs that rise faster than general inflation

- Might spend 20-30 years in retirement

Most retirement calculators and plans either skip inflation or underestimate how it affects long-term savings.

Why Ignoring Inflation Is a Mistake

Skipping inflation creates major problems for retirees. It drastically changes how much you can safely withdraw each year. Without adjusting for inflation, a 7% withdrawal rate might look fine over 30 years but drops to 4% when you factor in rising prices.

Inflation hits retirees harder than working adults. Retiree income rarely keeps pace with rising prices. Private sector pensions usually don’t adjust for inflation, so their real value keeps dropping.

Older households feel high inflation’s sting more sharply, though wealth levels make a difference. Wealthy households usually do better because they invest more in assets that grow with inflation. Lower-wealth retirees often depend on fixed-income investments that struggle during inflationary times.

The effects add up over time. Someone retiring with €477,105.06 today might see their money’s real value cut in half later in retirement if it doesn’t grow. This scenario makes inflation one of the biggest threats to your financial security in later years.

How to Avoid Ignoring Inflation in Retirement Planning

Here’s how to shield your retirement from inflation’s effects:

Consider diversifying your investments thoughtfully. A diverse portfolio helps protect against inflation risks. Think about:

- Stocks (they beat inflation over long periods)

- Real estate (property values and rents usually rise with inflation)

- Commodities like gold, oil, and farm products

Factor inflation into your retirement math. We use 2.5% inflation when looking at retirement goals. You might want to speak with us to update your plan if you expect higher long-term inflation.

Look into inflation-protected annuities. These products increase their payouts over time, helping offset how inflation affects your retirement income.

Keep your budget flexible. The traditional 4% withdrawal rule suggests taking 4% of your portfolio in your first retirement year, then adjusting that amount yearly for inflation. You might also want to set your optional spending as a range you can adjust when needed.

Note that inflation isn’t just some abstract concept – it’s a real force that touches every part of your retirement planning. Understanding the facts helps you avoid a costly mistake.

Not Planning for Long-Term Care

Image Source: Investopedia

Long-term care remains one of the most neglected parts of retirement planning. Studies indicate that at least 70% of 65-year-olds will need long-term care during their lifetime. Your biggest retirement planning mistake could be excluding this reality from your financial strategy.

Not Planning for Long-Term Care Explained

The lack of long-term care planning means you haven’t prepared financially to get help with daily activities like bathing, eating, or moving around as you age. Many people stay optimistic about their future health. About one-third over 65 worry they can’t afford care costs as they age. Yet they still don’t plan ahead.

Why Not Planning for Long-Term Care Is a Mistake

Your retirement savings can vanish quickly due to long-term care costs. The median assisted living stay lasts 22 months. That adds up to €123,856.47 at current rates. Memory care or extensive nursing support pushes these costs even higher.

Your family members might end up carrying your financial burden without proper planning. Women face the biggest impact. Their work lives change because of caregiving duties 60% of the time. Female carers lose €286,263.04 in lifetime earnings on average.

Nobody knows when they’ll need care. About 41% of households might run out of money in retirement with long-term care costs. The average monthly payment drops to 26% when these costs are excluded.

How to Avoid Not Planning for Long-Term Care

Here are your main options to think about:

- Traditional long-term care insurance: This type of plan offers the most complete coverage. Only 3 to 4% have these policies. Buy in your early 50s to get lower premiums.

- Hybrid policies: Life insurance with long-term care riders gives death benefits if you don’t need care. This option solves the “use-it-or-lose-it” issue of traditional policies.

- Self-insurance: People with very high net worth can set aside €0.95 million for care costs. This arrangement gives them flexibility without paying insurance premiums.

- Home equity options: A reverse mortgage or home sale could fund your care needs.

The best strategy often combines several approaches. Some families generate monthly income by renting their parent’s home to help with assisted living expenses. Others look at programs that offer limited help but usually have long waitlists.

Whatever path you take, we say you need a solid plan. When clients wait until a crisis hits, the options narrow, and the emotional toll spikes.

Relying on a Single Source of Income

Your retirement security faces serious risks if you put all your money into one investment. One in four individuals struggles with poverty because they lack sufficient diverse income sources to manage economic challenges.

Relying on a Single Source of Income Explained

A single income source means you depend on just one payment stream to fund your retirement. This source of income could be Social Security, a pension, or another asset. This approach makes you vulnerable to specific risks tied to that income type. Fixed income payments like pensions don’t keep up with inflation, which means your money buys less over time.

Why Relying on One Income Source Is a Mistake

The “sequence of returns risk” poses the biggest threat in early retirement. You might need to sell investments at low prices to cover expenses during market downturns. Such events can permanently damage your portfolio’s future.

Tax planning becomes more difficult with a single income source. Having diversification in income allows you to possibly pay less tax.

Different income sources protect you from different risks. Social Security adjusts for inflation but might not give you enough income by itself. Stocks can grow your money but move up and down with markets, making them risky as your only support.

How to Avoid Relying on a Single Source of Income

You can build multiple income streams by:

- Creating “buckets” for different expenses—use predictable income sources (Social Security, pensions, annuities) for essential needs and growth investments for extra spending

- Varying account types (pre-tax, tax-free, and taxable) to improve tax efficiency

- Building passive income through dividend-paying stocks, bonds, real estate, and other investments

- Keeping investments in any single asset class under 10%

- Mixing guaranteed income (pensions, annuities) with growth investments to curb inflation

This financial strategy provides you with stability and flexibility. It substantially improves your chances of keeping your lifestyle throughout retirement.

Comparison Table

| Retirement Planning Mistake | Key Statistics | Main Consequences | Main Solutions |

|---|---|---|---|

| Not Saving Early Enough | 1 in 5 individuals over 50 have no retirement savings; Average savings under 25 is €7,014.40 | Money loses the benefits of compound interest over time, so later contributions must be significantly higher. Starting at 40 versus 20 results in €1.34M less | Begin saving right away; Set up automatic savings; Take full advantage of employer matching; Yearly contribution increases of 1% help build wealth |

| Not Having a Retirement Spending Plan | 49% of retirees spend more than expected; 25% underspend due to uncertainty | Savings deplete faster than planned; Emotions drive financial choices; Changes become harder to handle | Essential and discretionary expenses need separation; Withdrawal rates should stay between 4% and 5%; Reviews happen every quarter; Different retirement phases need unique plans |

| Ignoring Inflation | 92% of retirees worry about inflation; 2% inflation cuts money value in half over 35 years | Money buys less over time; Withdrawal rates need adjustment; Fixed-income reliance hurts more | Assets need inflation protection; Social Security claims can wait; Inflation-protected annuities help hedge risk |

| Not Planning for Long-Term Care | 70% of people turning 65 will need long-term care | Retirement savings vanish quickly; Family shoulders the burden; Medicare coverage falls short | Long-term care insurance is most effective when purchased in the early 50s; hybrid policies provide flexibility; and self-insurance funds can be beneficial. |

| Relying on a Single Source of Income | 25% of older adults face poverty from lack of income variety | Market downturns hit harder; Tax planning becomes limited; Options stay restricted | Multiple income streams create safety; Account types need variety; Passive income helps stability; Single assets should stay under 10% |

Conclusion

Your financial security during retirement can substantially improve by avoiding these five costly planning mistakes. A solid retirement plan helps ensure the lifestyle you want after leaving work. Many people miss key aspects of their financial future, but knowing these common pitfalls is your first step toward building a more secure retirement.

Building financial security takes more than just saving money. Your retirement strategy should cover multiple areas – from healthcare planning to protecting against inflation. Starting early and creating different income streams gives you big advantages through compound interest and market cycles. The choices you make decades earlier often determine whether you’ll have a comfortable retirement or face financial stress.

The numbers tell us a lot—70% of people who turn 65 will just need long-term care, but very few prepare well for this reality. People also underestimate healthcare costs by over €85,000, which leaves retirees vulnerable when they need stability most. These facts show why detailed planning matters deeply.

Smart retirement planning looks carefully at spending patterns, inflation effects, and how long you might live. Reviewing your plan every three months helps ensure you stay on track, regardless of any economic changes or personal situations that may arise. We help successful expats and business owners, and we provide flexible insurance solutions for organisations that want to grow.

To ensure a successful retirement plan, we encourage you to take action now. Each mistake you avoid could save you thousands and reduce stress during retirement. Your future comfort depends on smart planning today, not luck. Take control of your retirement destiny – your future self will definitely thank you.